We won’t get a second shot at this.

The life insurance industry faces a once-in-a-generation opportunity to fundamentally change how we do business and how consumers feel about how we do business.

The situation today is dire. Some 31% of consumers decline to purchase life insurance because they don’t trust insurance companies, according to the 2018 LIMRA Insurance Barometer Survey.

Note the subtext in that number. Consumers aren’t saying they don’t need insurance. Or that they can’t afford it. They’re saying they don’t trust our industry.

Yet as clear and disturbing as that may be, consumers are also demonstrating a willingness, even an eagerness, to learn to trust us.

Consider if you will this year’s version of the LIMRA Insurance Barometer Survey, in which 47 percent of Americans surveyed said they are more likely to buy life insurance using some type of “simplified” underwriting. And of that group, more than half (57 percent) cited “risk and price transparency” as key to their reasoning. Furthermore, Accenture’s 2019 Global Financial Services Consumer Study shows that 75 percent of consumers across the world are willing to share more data with insurers if it leads to lower prices.

Opaque processes vs. simplified underwriting

Data, machine learning, algorithms. The insurance industry has become quite excited by these ideas. And with good reason. State-of-the-art, risk-based solutions promise us a more efficient future as an industry that better understands how to price risk.

But there are even bigger opportunities than improved efficiency to be found. By fundamentally changing how consumers interact with us we can fundamentally change how consumers feel about us.

Or, as the LIMRA surveys show: more consumers will buy life insurance if they trust us, and more consumers will trust us if we embrace transparency.

We’re an open book

At LifeScore Labs, we’ve made a business decision to advocate for consumers. We want to do more than just appear to be on consumers’ side. We want to do more than simply market ourselves as having consumers’ interests at heart.

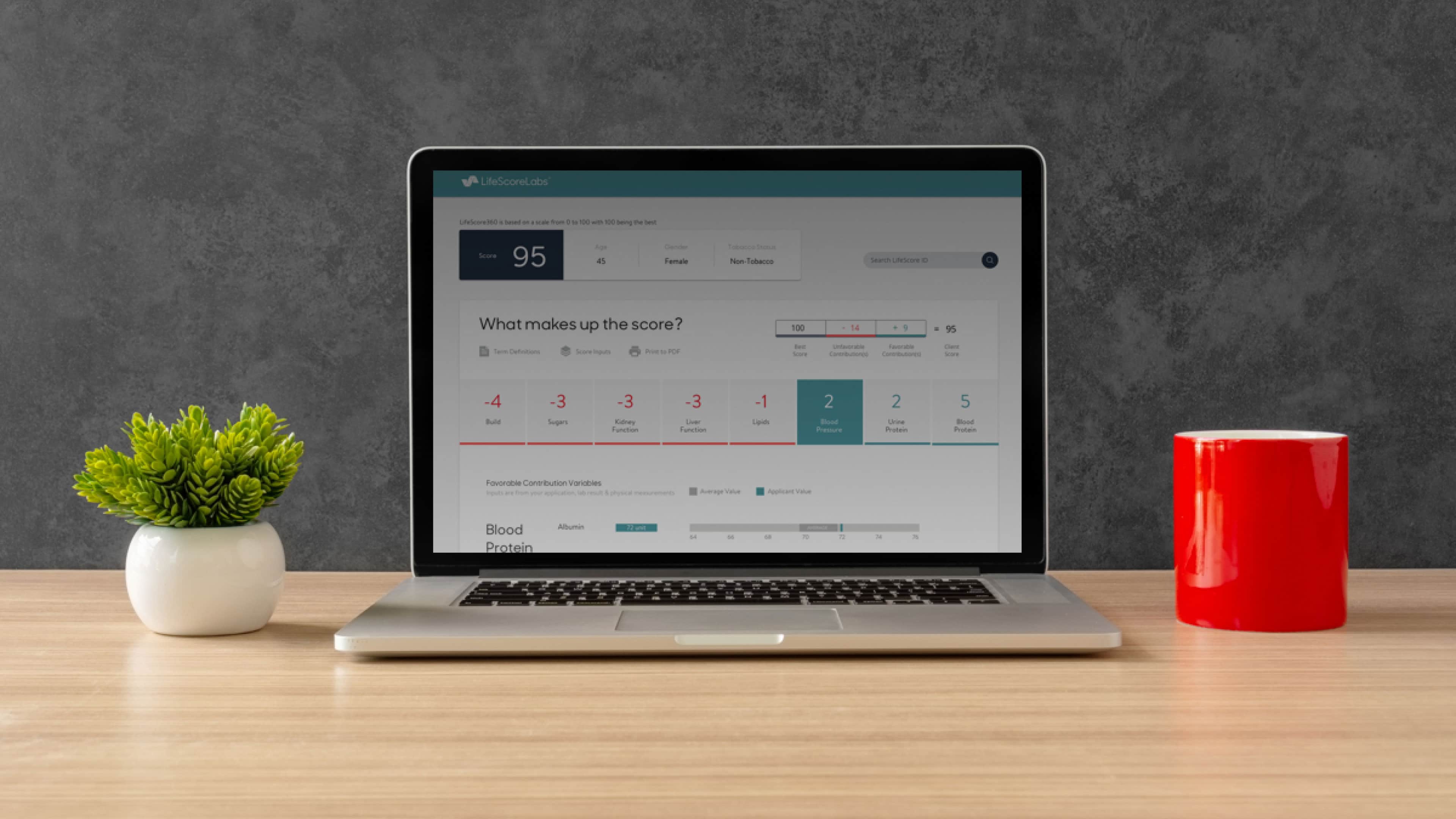

For example, MyLifeScore is a white-labeled, consumer-facing, simplified version of our flagship risk-scoring , LifeScore Med360. It is designed to show an individual how their life insurance risk is measured, and where they score in relation to their peers. Knowing their score can help consumers better understand what the insurance-buying process may look like for them.

It is one of the first in a series of steps we’re taking to help make life insurance underwriting transparent to potential customers.

Because transparency builds trust.

Fairness

To truly win consumers’ trust, our industry should first demonstrate to the public that today’s data-driven risk-scoring models will treat consumers fairly.

And here again transparency points the way forward.

As we enter this new era of data and machine learning, our industry should work to ensure our models yield unbiased results and do not discriminate unfairly.

Getting the future right

The future of insurance is here. Machine learning, algorithms, big data, etc. point the way forward. But they are not a guarantee of prosperity for insurers.

It is quite possible that we as an industry will take too long to embrace a new approach of consumer advocacy and transparency.

If our industry is unwise, we will let the future be built by third parties or someone without an interest in the success of our industry and the consumers we serve.

But If we are wise, we will build the future ourselves using the LifeScore Labs model or something like it.

The time to decide is now. We won’t get a second shot at this.

CRN202109-253311